After GAC Compliance Audit- July 1, 2018-December 31, 2024

PHOTO: Breakdown of the amount that can’t be traced (above) and Liberia’s Auditor General, P. Garswa Jackson (below)

NEWS AN ANALYSIS BY Frank Sainworla, Jr., newspublictrust@gmail.com

Once again, the General Auditing Commission (GAC) has done its job to identify financial and other accountability and transparency lapses in the Liberian government bureaucracy in the ongoing fight against corruption and weak governance practices.

The latest of such reports is its recent release of its compliance audit on the Special Reconciliation of Government Tax collected from July 1, 2018-December 21, 2024.

What the GAC audit has uncovered is Unauthorized withdrawals of tens of millions of United States dollars— US$278 million and over L$23 billion—but the million dollar-question is: Who did them and what will be done to such officials?

After many decades of impunity both through war crimes and crimes against humanity and economic crimes, is it unfair to call for not only a swift investigation and implementation of the GAC’s recommendations, but holding officials responsible for the discrepancies accountable?

The period of this audit spans two administrations—the former ruling CDC government of ex-President George Manneh Weah and ruling Unity Party “rescue” government of current President Joseph Nyuma Boakai.

This latest GAC report is among 25 other rigorous audit reports that the Auditor General’s office has released in recent time—ranging from compliance audit to other investigative/management audits. Given the huge amounts of tax payers’ money that appears to be elusive, one political analyst recently intimated to this writer that “officials responsible must be made to account”.

In a letter dated April 2026 addressed to the current Finance Minister, Augustine Ngafuran, Liberia’s Auditor General, P. Garswa Jackson said:

“We have undertaken a Compliance audit on the Special Reconciliation of the Government Tax Revenue Collected through the Government Transitory Bank Accounts and the Consolidated Accounts for the fiscal periods July 1, 2018 to December 31 2024. The Special Reconciliation was conducted in line with Section 2.1.3 of the General Auditing Commission (GAC) Act of 2014.”

The Auditor General added: “Given the significance of the matters raised in this report, we urge the Honourable Speaker and Members of the House of Representatives and the Honourable Pro- Tempore and Members of the Liberia Senate to consider the implementation of the recommendations conveyed in this report with urgency.”

As good and independent Journalism is to promote the public good and public interest, this news outlet here highlights some of the key points raised in the GAC audit.

In this audit report, the Auditor General’s position is clear: “Management assertion did not adequately address the issues raised. Management did not account for the unmatched revenue receipts as requested…Management also did not provide a reconciliation report of the unmatched revenue receipts…”

But ultimately: Who Pays For Nearly US$278M And Over L$23Bn That “Could Not Be Traced To Transitory Bank Account?

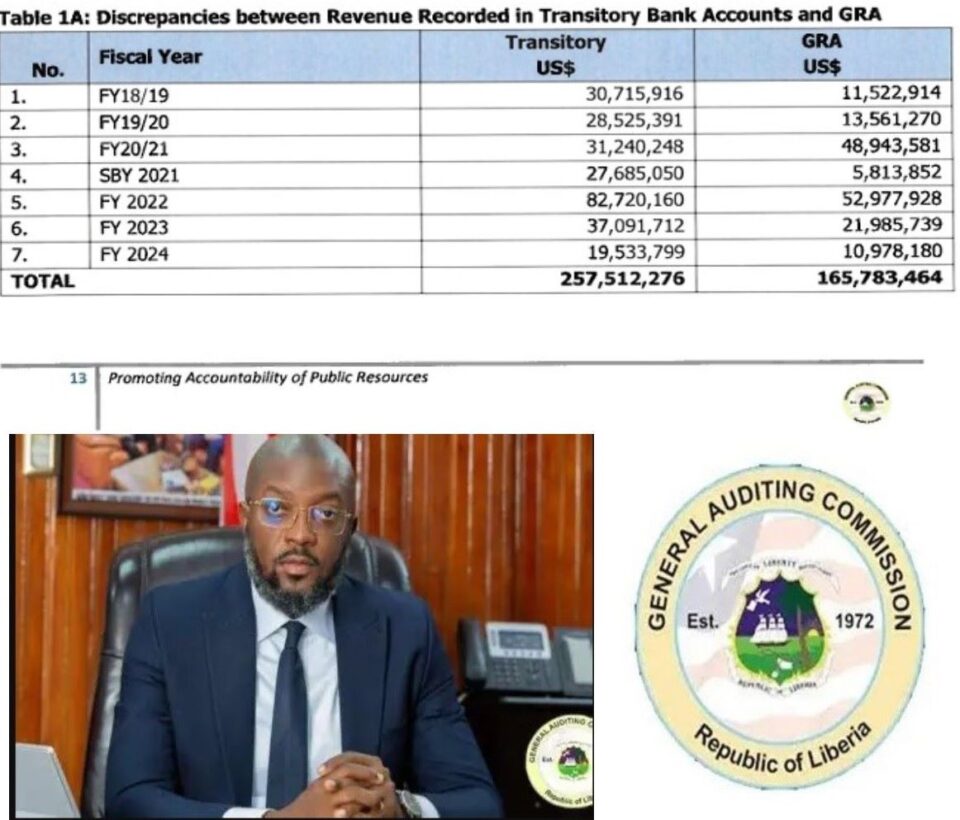

Discrepancies between Revenues Recorded in Transitory Bank Accounts and GRA (General Revenue Account)

1.1.1.3 During the audit, we observed total revenue amounting to US$257,512,276 and

$23,633,186,485 recorded in the transitory bank accounts could not be traced to the General Revenue Accounts (GRA). Similarly, we observed total revenue from the transitory bank accounts recorded in the GRA amoun’ing to US$ 165,783,464 and could not be traced to the transitory bank accounts.

What lapses the compliance audit found:

- Discrepancies between- Revenue Res.-dec. Ban; Accunts and GRA Total revenue amounting to and $23,633,186,485 recorded in the transitory bank accounts could not be traced to the General Revenue Accounts (GRA). Similarly, total revenue from the transitory bank accounts recorded in the GRA amounting to US$165,783,464 and could not be traced to the transitory bank accounts.

Discrepancies

Total revenue receipts amounting to US$1,789,395,225.27 and recorded in the

- Tax Administrative System (TAS) could not be traced to the General Revenue Account (GM). Similarly, total revenue receipts recorded in the GRA amounting to and $68,392,483,222.46 could not be traced to the TAS. Further, because we could not reconcile the unmatched transactions in the TAS to the unmatched transactions in GRA, we summed up the total matched and unmatched transactions per the TAS and reconciled same to the total matched and unmatched transactions per the GRA resulting into variances amounting to (US$373,919,113.26) and

- Unauthorized Withdrawals

There were several unauthorized withdrawals amounting to I.JS« 59,786.14 and I-$ 551,773.87 in the transitory accounts for the periods under audit. These transactions were classified as othe- debits Other debits relate to transactions that we could not categorized under any of the previously defined classes of approved debit transactions. Other debits included “school fee deducted, suspended fees payment – online transfers, etc”.

Other irregularities uncovered:

The following irregularities are associated with the collection of revenue at rural customs and tax collectorates

No evidence of expansion, installation, and operationalization of ASYCUDA and I-ITAS automated revenue reporting software at rural collectorates to facilitate comprehensive, realtime and accurate recording of revenue generated/collected. Bills are manually raised for subsequent payment of taxes.

i Taxes are paid in cash and cash paymentç from various tax payers were maintained by tax collectors for protracted periods.

- Cash payments collected from tax payers are subsequently deposited in bulk as a single transaction.

- Various bills and payments of taxes were subsequently reported as bulk transactions in the ASYCUDA and LITAS.

- No evidence of reconciliation among bills manually raised, cash collected, cash subsequently deposited and bills and payments recorded in the ASYCUDA and I-ITAS where applicable.

GAC recommendations:

1.1.1.10 Management should facilitate daily automated reconciliation among the TAS, Transitory I (Revenue) bank accounts at commercial banks, GRA and the created Revenue module in IFMIS. Variances identified should be investigated and adjusted where applicable in a timely manner- Evidence of periodic reconciliation reports should be adequately documented and Ifiled to facilitate future review.

1.1.2.10 Going forward, Management should ensure that all receipts of revenue and tax payments are preceded by the creation of bills or invoices through the appropriate tax systems (‘ TTAS and ASYCUDA) before deposits of funds in the GRA The GRA should be automatediy linked to •tne TAS such that as payments are received in the GRA, the TAS is automatically updated.

1.1.2.11 Management should facilitate the establishment of a revenue! cash receipt module in the IF-MIS to adequately capture actual revenue received during the period. The created revenue module should be automatedly linked with the TAS and the GRAs to facilitate real time and accurate recording of revenue.

1.1 2 12 Management should facilitate daily automated reconciliation among the TAS, Transitory (Revenue) Accounts at commercial banks, GRA and the created Revenue module in IFMIS. Variances identified should be investigated and adjusted where applicable in a timely manner.

Risk observed during the GAC audit:

Risk

1.1.3.3 The absence of unique identifiers for all bills and payments in ASYCUDA may impair effective review and reconciliation of revenue receipts.

1.1.3.4 Bills may be raised in the systems without evidence of payments. This may lead to under collection of revenue and misappropriation of public funds.

- 1.3.t-Illegitimate payments may be recorded in the systems. This may lead to fraudulent financial reporting and misappropriation of public funds.